Rural Land – A Compelling part of a Diversified Investment Strategy

Our “Geopolitics, Trade Volatility, and Rural Land Investment” article outlined how rising geopolitical risk, inflation pressure, and trade disruption are reshaping the global investment landscape. In such environments, investors increasingly focus not only on expected returns, but on how assets behave during periods of market stress. It showed that farmland can serve as a genuine portfolio diversifier during periods when geopolitical events create synchronised stress across equity and bond markets.

This article examines the investment evidence underpinning rural land as an asset class, drawing primarily on long-running United States institutional datasets that are widely used by global investors. While New Zealand Rural Land Company’s (NZL’s) assets are located in New Zealand, the underlying economic characteristics of farmland are structurally similar across developed agricultural markets, making US institutional evidence relevant for assessing farmland’s role within diversified portfolios.

A Changing Investment Landscape

Historically, diversification in agriculture meant spreading risk. Today, it’s the engine of growth. Globally, investors are allocating more capital to productive land as a strategic asset class - a scarce real asset with demonstrated resilience in inflationary environments, that also stores carbon and supplies a growing population with food.

Since 2020, institutional capital has shifted heavily toward tangible, inflation-linked assets[1]. Infrastructure funds are now the fastest-growing segment of global private markets, reflecting investors’ search for inflation protection and yield stability[2]. Agricultural land, with similar inflation-hedging characteristics, is following suit[3].

The evidence consistently demonstrates that farmland exhibits lower volatility, stronger inflation-hedging characteristics, and near-zero correlation with traditional asset classes, making it an effective portfolio diversifier both globally and in New Zealand.

Farmland as a Distinct Asset Class

Farmland differs fundamentally from traditional financial assets. Returns are derived from two sources:

Income returns, generated through agricultural production or rental income, and

Capital appreciation, driven by land scarcity, productivity gains, and inflation over time.

Because these drivers are largely independent of corporate earnings cycles or interest-rate movements, farmland returns have historically shown low correlation with equities and bonds. This characteristic becomes particularly valuable during periods when traditional diversification breaks down, such as inflationary or geopolitical shocks.

Institutional farmland performance in the United States is most commonly measured using the NCREIF Farmland Index, which tracks professionally managed farmland held by pension funds, endowments, and insurance companies. This index provides one of the longest and most robust datasets available for analysing farmland as an investment asset.

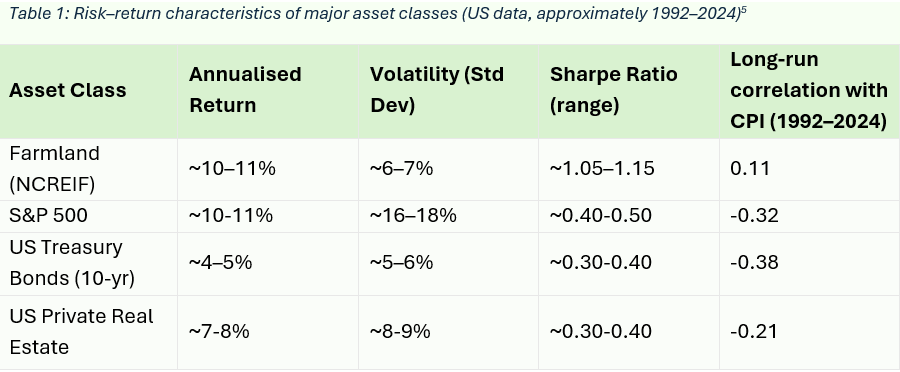

Risk, Return, and Volatility

Over multi-decade periods, US farmland has delivered equity-like total returns with materially lower volatility. According to NCREIF data, farmland has generated long-term annualised returns of approximately 9–11%, with volatility typically in the range of 6–7%[4]. By comparison, US equities have delivered similar long-run returns but with substantially higher volatility, while bonds have exhibited lower volatility but materially lower returns. This combination positions farmland favourably on a risk-adjusted basis. Sharpe ratios shown below are calculated using total returns relative to the prevailing risk-free rate. These figures indicate that farmland has historically delivered higher returns per unit of risk than both equities and bonds over full cycles.

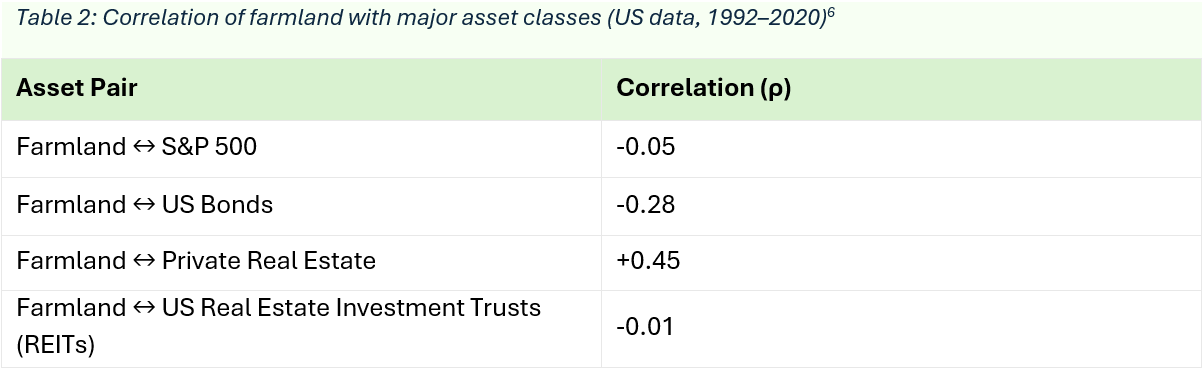

Diversification Benefits: Correlation with Traditional Assets

Returns alone do not capture how assets behave together within a portfolio. A key advantage of farmland is the degree to which its returns move independently of traditional financial markets. Publicly available analysis by FarmTogether, drawing on NCREIF farmland data and standard market benchmarks, reports the following long-run correlations based on annual total returns from 1992-2020.

These correlations highlight farmland’s ability to provide genuine diversification, particularly in environments where equities and bonds have become more closely correlated — a trend observed in recent years. Near-zero correlation with equities (S&P 500) indicates farmland returns are largely independent of stock market cycles. A negative correlation with bonds suggests farmland can provide diversification when fixed income underperforms, such as during inflationary or rising-rate environments. Moderate positive correlation with private real estate reflects shared characteristics as income-generating, illiquid real assets.

Inflation protection

Farmland’s inflation-hedging properties are not incidental. Rising inflation tends to increase food prices over time, raise the replacement cost of land and infrastructure, and support nominal agricultural incomes. Over the full 1992–2024 period, farmland exhibited a modest positive correlation with CPI (0.11), indicating that it does not simply track inflation year-to-year. However, a longer-term analysis (1910–2025) shows a much stronger correlation of +0.67 between farmland and CPI.

However, this long-run average masks important dynamics. During inflationary shocks — such as the post-COVID period — farmland has tended to preserve real value and outperform financial assets, particularly bonds, which exhibit a strongly negative correlation with CPI (0.38). In 2022, when US CPI inflation averaged approximately 8%[7], institutional farmland delivered a total return of around 11–12%[8] (primarily from income returns), as measured by the NCREIF Farmland Index, outperforming bonds and preserving real value during an inflationary shock.

Because farmland tends to have a positive correlation with the CPI it is an attractive asset class for investors seeking to hedge against inflationary periods, especially relative to assets with a negative correlation.

Relevance for New Zealand Investors

While the datasets referenced above are US-based, the underlying drivers of farmland performance, land scarcity, essential demand for food and fibre, income-based returns, and inflation sensitivity, are common across developed agricultural economies, including New Zealand.

New Zealand farmland has historically delivered competitive long-run returns, with studies such as Eves and Painter (2008)[9] reporting average annual returns of approximately 14% over the period 1990–2005, driven by a combination of income and capital appreciation. More recently, regulatory uncertainty and capital constraints have limited land price growth, sharpening the focus on operating returns which have caught up and remained strong.

From an investment perspective, this divergence reinforces the role of farmland as an incomegenerating, real asset that can continue to perform even when capital values are subdued.

Summary

Taken together, the evidence suggests that farmland offers a combination of risk-adjusted returns, inflation protection, and diversification benefits that are increasingly difficult to replicate in traditional asset classes. These characteristics underpin the strategic role of rural land within diversified investment portfolios. For New Zealand investors, local farmland offers these benefits with the added potential for capital appreciation as market conditions normalise. The following article builds on this foundation by examining how diversification across rural land uses can further enhance resilience and long-term performance within a rural land portfolio.

Carla Muller

Principal Consultant, Perrin Ag.

Published January 2026

[1] Preqin. (2024). 2024 Global Infrastructure Report. Preqin Ltd.

[2] BlackRock. (2024). Global Private Markets Outlook 2024. BlackRock Alternatives Institute.

[3] Craigmore Partners. (2024). The potential returns on New Zealand land. https://www.craigmore.com/the-potentialreturns-on-new-zealand-land

[6] https://farmtogether.com/learn/blog/farmland-high-returns-low-volatility-critical-role

[7] Federal Reserve (FRED) – CPI-U https://fred.stlouisfed.org/series/CPIAUCSL

[9] Eves, C., & Painter, M. (2008). Eves, Chris and Painter, Marvin (2008) A comparison of farmland returns in Australia, Canada, New Zealand and United States. Australian & New Zealand Property Journal, 1(7). pp. 588-598

The opinions and views expressed in this article are the author's own and do not necessarily reflect the views and opinions of New Zealand Rural Land Company Limited or its Board of Directors.